- Yokohama-shi Top Page

- Living and Procedures

- family register Tax and Insurance

- Taxes

- City tax of Yokohama

- Individual municipal tax and prefectural tax

- Individual Municipal Tax and Prefectural Tax (Details)

- About special tax credit (fixed tax reduction) of individual municipal inhabitant tax and prefectural inhabitant tax for 2024

Here's the text.

About special tax credit (fixed tax reduction) of individual municipal inhabitant tax and prefectural inhabitant tax for 2024

Last Updated June 27, 2024

- Overview

- Target person

- Calculation method

- Procedure

- Confirmation method

- Implementation method

- Notes

- Those who are not eligible

- Benefits

- Related information

- FAQs

- To businesses (special collection obligations)

Please refer to the list at the bottom of the page for details.

[We do not notify Yokohama City of fixed-rate tax cuts by e-mail or other means]

Please note that even if you receive an e-mail that claims to be Yokohama City, it is considered to be the purpose of fraudulent information. If you receive an unrecognized email, please delete it immediately without accessing the URL described in the email or entering personal information.

In addition, by telephone from Yokohama City, cut out "Because you can receive a refund due to fixed tax cuts" or "I will transfer benefits" and ask for personal information (bank account number, PIN, my number, etc.) Please note that we do not go.

1 Overview

As a temporary measure to mitigate the burden on people whose wage increases have not kept up with prices and to realize an economy in which sustainable wage increases are sufficiently high, individual municipal tax and prefectural tax special tax credits (hereinafter referred to as "fixed tax reduction") will be implemented.

2 Target persons

Taxpayers whose total income pertaining to personal residence tax for fiscal 2024 is 18.05 million yen or less

(In the case of salary income only, taxpayers with salary income of 20 million yen or less (20.15 million yen or less for those who are eligible for income adjustment deduction for children and special disabled persons, etc.))

※Not applicable if the taxpayer's tax amount calculated without including the fixed amount tax reduction is less than the per capita rate (6,200 yen).

Details of those who are not eligible

3 Calculation Method

The following amount is deducted from the income percent after tax credit for the taxpayer's personal residence tax. (If the deduction exceeds the person's income percent, the income percent will be the limit.)

The same living spouse (excluding foreign residents) excluding spouses subject to deduction is not eligible for the fixed amount tax reduction in FY2024, of which domestic residents are subject to personal residence tax in FY2025. 10,000 yen will be deducted from the income percent.

(1) 10,000 yen

(2) ¥ 10,000 per deductible spouse (excluding foreign residents) or dependent relatives (excluding foreign residents)

Example: Fixed amount tax reduction for taxpayers, deductible spouses, and two dependent children

10,000 yen (person) + 3 people x 10,000 yen = 40,000 yen

4 Procedures

The fixed amount tax reduction is calculated based on tax information held by Yokohama City (final tax return, resident tax return, salary payment report, pension payment report, etc.).

There is no need to apply for a fixed amount tax reduction.

5 Confirmation Method

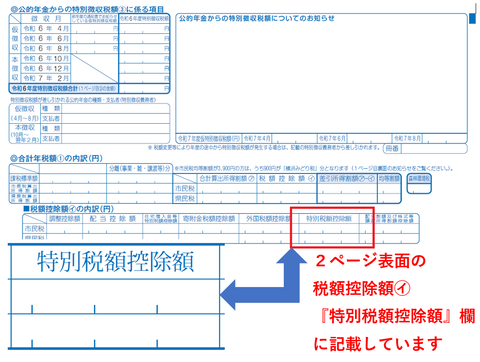

The fixed amount tax reduction can be confirmed in various notices of personal residence tax.

※There has been no change in the timing of notification.

In the case of normal collection or special collection from public pension (scheduled to be sent to individuals around early June 2024)

"2024 municipal tax, prefectural tax, forest environmental tax amount determination tax payment letter of advice"

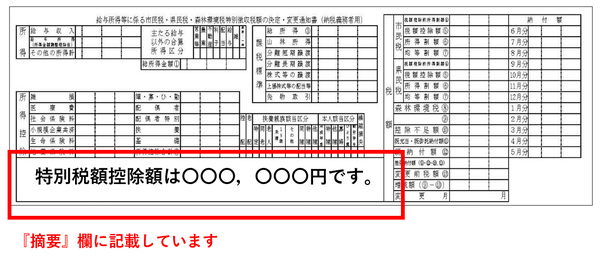

In the case of special collection from salary (scheduled to be distributed from your employer around late May 2024)

"Determination / change notice of municipal tax, prefectural tax, forest environmental tax special collection tax amount pertaining to salary income in 2024 (for taxpayers)"

Paper sent

Electronic delivery

6 Implementation Method

The method of implementing the fixed amount tax reduction varies depending on the method of paying personal residence tax.

※ For those who are not eligible for the fixed-rate tax reduction, there is no change in the past.

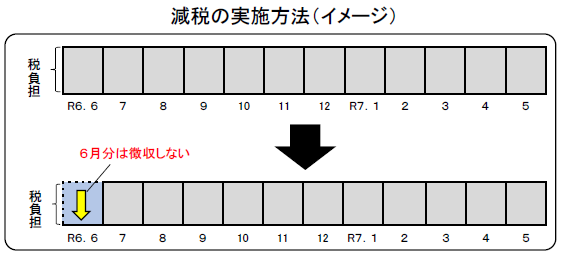

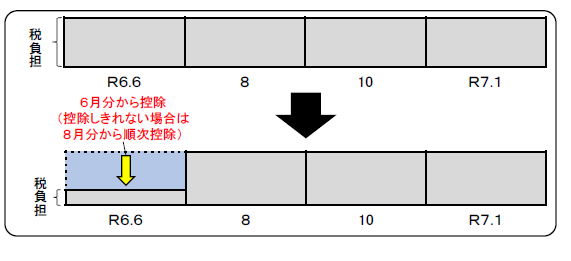

Person whose personal residence tax is deducted from salary (special collection)

When paying salaries in June 2024, no special collection will be made, and the amount of personal residence tax and forest environmental tax after deducting the amount of fixed tax reduction will be collected from July 2024 to May 2025. Collect in 11 separate installments.

※ Those who are not eligible for the fixed amount tax reduction will be collected in 12 separate installments from June 2024 to May 2025 as before.

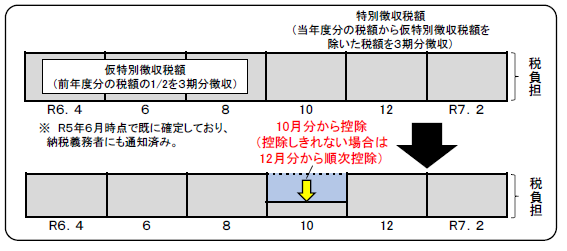

Person who deducts personal residence tax from public pension (special collection of pension)

The amount equivalent to the fixed amount tax reduction is deducted from the amount of personal residence tax and forest environmental tax that should be specially collected for public pension, etc., which is first paid by the Minister of Health, Labor and Welfare, etc. after October 1, 2024 (hereinafter referred to as the special collection tax amount for each month). In addition, if the deduction exceeds the special collection tax amount for each month, the amount equivalent to the special collection tax amount for each month will be deducted, and the amount of the part that cannot be deducted even after deducting will be deducted from the special collection tax amount for each month specially collected during the year.

Those who pay by payment slip and fund transfer (normal collection)

Amount equivalent to the amount of fixed tax reduction from the amount paid for the first term pertaining to personal residence tax and forest environmental tax for 2024 (if the amount exceeds the amount paid for the first term, The amount equivalent to the payment amount for the first term) is deducted. In addition, the amount of the portion that cannot be deducted even after deducting from the first term will be deducted sequentially from the payment amount after the second term.

7 Notes

Since the income percent for fiscal 2024, which is the basis of the next calculation, is calculated based on the income percent before the fixed tax reduction, there is no effect of the fixed tax reduction.

- Deduction limit of exception deduction of oldness and tax payment

- pension Special Collection Tax Amount (April, June and August 2025)

8 Those who are not eligible

In the case of the person

Those whose total income pertaining to personal residence tax for 2024 exceeds 18.05 million yen

(In the case of only salary income, taxpayers who exceed salary income of 20 million yen (more than 20.15 million yen for those who are eligible for income adjustment deduction for children and special disabled persons, etc.))

Those whose tax amount calculated without including fixed tax reduction is less than the per capita rate (6,200 yen)

In the case of addition

Deductible spouses residing outside the country

Dependent relatives residing outside the country

Same living spouses excluding spouses subject to deduction (because they are eligible for FY2025, they are not eligible for FY2024)

How to collect the special collection tax amount for those who are not eligible

For those who are not eligible due to income requirements, those who have calculated without including fixed tax cuts are less than the per capita rate (6,200 yen), special collection will be made from June as before.

9 Benefits

Benefits (adjustment benefits) for those who are not expected to be able to reduce the fixed amount.

In the 2024 personal residence tax, the calculated tax reduction amount (fixed tax reduction amount) exceeds the personal residence tax income percent before the fixed tax reduction, and if it is expected that the fixed tax reduction cannot be completed, adjustment benefits will be made.

Please refer to the following page for details.

Adjustment Benefits

※ For those who are eligible for the adjustment benefits, a "news of payment" or "confirmation letter" will be sent out sequentially from Monday, July 22, 2024.

[Contact information regarding adjustment benefits]

Yokohama City Electric Power, Gas, Food and Other Prices Emergency Support Benefit Call Center

Telephone: 0120-045-320

Fax: 0120-303-464 (for hearing-impaired inquiries)

Email address: support@yokohama-kyufu.jp

Benefits to newly-exempt households

In the 2024 personal residence tax, only those who are newly exempt from the personal residence tax per capita rate or those who are not subject to the personal residence tax income rate, 100,000 yen per household will be paid.

In either case, 50,000 yen per elementary school student will be paid if the household has elementary school student under the age of 18.

※ However, this does not apply if all households are dependent on other relatives who are subject to personal residence tax.

※ If you are eligible for tax-exempt households in 2023, you will not be eligible for the 2024 benefit.

Please see the next page for benefits to households that are newly exempt from tax.

Information on benefits [100,000 yen] + child addition [50,000 yen] to households where the residence tax was newly exempt and only the per capita rate was taxed in 2024.

※ "news of payment" or "confirmation letter" will be sent out sequentially to households eligible for payment of benefits from Wednesday, July 24, 2024.

[Contact for benefits to newly-exempt households]

Yokohama City Electric Power, Gas, Food and Other Prices Emergency Support Benefit Call Center

Telephone: 0120-045-320

Fax: 0120-303-464 (for hearing-impaired inquiries)

Email address: support@yokohama-kyufu.jp

10 Related Information

In the future, it will be released as soon as information by the government is released.

[Reference] Ministry of Internal Affairs and Communications Tax System Revision (Local Tax) (External Site)

Please refer to the following page for information on the fixed income tax reduction.

11 Frequently Asked Questions

It is posted on this page.

Frequently Asked Questions about Fixed Income Tax Reduction

12 Towards businesses (special collection obligations)

Click here for a document that summarizes the points related to fixed tax reduction for businesses (special collection obligations).

News from Yokohama-shi about fixed amount tax reduction (PDF: 3,791KB)

Contact information

If you have any questions, please contact each ward office.

| Ward office | Window | Phone number | E-Mail address |

|---|---|---|---|

| Aoba Ward | 55th floor on the 3rd floor of Aoba Ward Office | 045-978-2241 | ao-zeimu@city.yokohama.jp |

| Asahi Ward | 28th floor, 2nd floor of Asahi Ward Hall Main Building | 045-954-6043 | as-zeimu@city.yokohama.jp |

| Izumi Ward | 304, 3rd floor of Izumi Ward Office | 045-800-2351 | iz-zeimu@city.yokohama.jp |

| Isogo Ward | 34th floor, Isogo Ward Office, 3rd floor | 045-750-2352 | is-zeimu@city.yokohama.jp |

| Kanagawa Ward | 325 on the 3rd floor of Kanagawa Ward Hall Main Building | 045-411-7041 | kg-zeimu@city.yokohama.jp |

| Kanazawa Ward | 304, 3rd floor of Kanazawa Ward Office | 045-788-7744 | kz-zeimu@city.yokohama.jp |

| Konan Ward | 31st floor, Konan Ward Office, 3rd floor | 045-847-8351 | kn-shiminzei@city.yokohama.jp |

| Kohoku Ward | 31st floor, Kohoku Ward Office, 3rd floor | 045-540-2264 | ko-zeimu@city.yokohama.jp |

| Sakae Ward | 30th floor, 3rd floor of Sakae Ward Hall Main Building | 045-894-8350 | sa-zeimu@city.yokohama.jp |

| Seya Ward | 33rd floor, Seya Ward Office, 3rd floor | 045-367-5651 | se-zeimu@city.yokohama.jp |

| Tsuzuki Ward | 34th floor, Tsuzuki Ward Office, 3rd floor | 045-948-2261 | tz-zeimu@city.yokohama.jp |

| Tsurumi Ward | No. 2 on the 4th floor of Tsurumi Ward Office | 045-510-1711 | tr-zeimu@city.yokohama.jp |

| Totsuka Ward | 72th floor, Totsuka Ward Office, 7th floor | 045-866-8351 | to-zeimu@city.yokohama.jp |

| Naka Ward | 43rd floor on the 4th floor of Naka Ward Office Main Building | 045-224-8191 | na-zeimu@city.yokohama.jp |

| Nishi Ward | 44th floor, Nishi Ward Office, 4th floor | 045-320-8341 | ni-zeimu@city.yokohama.jp |

| Hodogaya Ward | 26th floor, 2nd floor of Hodogaya Ward Hall Main Building | 045-334-6241 | ho-zeimu@city.yokohama.jp |

| Midori Ward | 35th floor, Midori Ward Office, 3rd floor | 045-930-2261 | md-zeimu@city.yokohama.jp |

| Minami Ward | 33rd floor, Minami Ward Office, 3rd floor | 045-341-1157 | mn-zeimu@city.yokohama.jp |

※For inquiries from special collection obligations regarding special collection, please contact the following.

Finance Bureau Corporate Taxation Division Special Collection Center

Telephone: 045-671-4471

Email address: za-tokucho@city.yokohama.jp

※In Yokohama, individual taxation work is carried out at each ward office Tax Division.

If you have any questions about the fixed amount of tax reduction for individual taxation details, please contact your ward office Tax Division listed on this page.

You may need a separate PDF reader to open a PDF file.

If you do not have it, you can download it free of charge from Adobe.

![]() To download Adobe Acrobat Reader DC

To download Adobe Acrobat Reader DC

Inquiries to this page

Tax Division, Chief Tax Department, Finance Bureau (I cannot answer consultations on individual taxation details and declarations.) Please contact your ward office Tax Division.)

Telephone: 045-671-2253

Telephone: 045-671-2253

Fax: 045-641-2775

Email address: za-kazei@city.yokohama.jp

Page ID: 555-786-588