- Yokohama-shi Top Page

- Living and Procedures

- family register Tax and Insurance

- Taxes

- City tax of Yokohama

- Individual municipal tax and prefectural tax

- About donation tax credit (hometown tax payment)

Here's the text.

About donation tax credit (hometown tax payment)

Last Updated September 20, 2024

Calculation of donation tax credit

◆Calculation method of donation tax credit (when we do not use oldness and tax payment one-stop exception system)

(a) Donations to prefectures and municipalities (subject to special deductions), (a) certain donations to community fundraising associations in the Address area or branches of the Japanese Red Cross Society, (c) donations to prefectures and municipalities (except for special deductions), (d) donations to organizations designated by Yokohama City by ordinance, and (e) donations to organizations designated by Kanagawa Prefecture (outside sites), municipal tax and prefectural tax are calculated based on the following methods.

●Basic Deductions

Municipal tax…("Total amount of (a), (a), (c) and (d) above or "30% of gross income, etc."-2,000 yen) x 8%

Prefectural tax…("Total amount of (a), (a), (c) and (e) above" or "30% of gross income, etc. "-2,000 yen") x 2%

●Special deduction (only hometown tax payment applies)

Municipal tax…The lesser of "(a) amount-2,000 yen) x deduction ratio (*) x 4/5" or "Municipal tax income percent (after deduction of adjustment deduction) x 20%"

Prefectural tax…The lesser of "(a) amount-2,000 yen) x deduction ratio (*) x 1/5" or "Prefectural tax income percent (after deduction of adjustment deduction) x 20%"

(※) Please refer to the table below. The taxable gross income amount refers to the taxable gross income amount of municipal tax and prefectural tax.

●Calculation method of deduction ratio

| Total amount of difference between taxable gross income (*1) and personal deduction from income tax (*2) | Deduction ratio |

|---|---|

| If it is less than 0 yen | 0.9(Note:) |

| 0 yen or more and 1.95 million yen or less | 0.84895 |

| More than ¥1.95 million and less than ¥3.3 million | 0.7979 |

| More than 3.3 million yen and less than 6.95 million yen | 0.6958 |

| More than 6.95 million yen 9 million yen | 0.66517 |

| More than 9 million yen and less than 18 million yen | 0.56307 |

| More than 18 million yen 40 million yen | 0.4916 |

| More than 40 million yen | 0.44055 |

(※1) The taxable gross income amount refers to the taxable gross income amount of municipal tax and prefectural tax.

(※2) Please see this page for the difference between personal deductions from income tax.

(Note) If the difference between personal deductions is greater than the gross taxable income, or if you have taxable forest income, taxable Retirement income, or income subject to special taxation, a different percentage will be applied. For more information, please contact your ward office, Tax Division City Tax Section.

◆About view of income percent of municipal tax, prefectural tax

The income percent of municipal tax and prefectural tax is listed in the municipal tax / prefectural tax tax payment letter of advice or the special collection tax amount letter of advice.

The amount of income percent of municipal tax and prefectural tax is determined by the situation such as the income of the previous year.

Therefore, it may differ from the amount stated in the notice, so please refer to it as a guide.

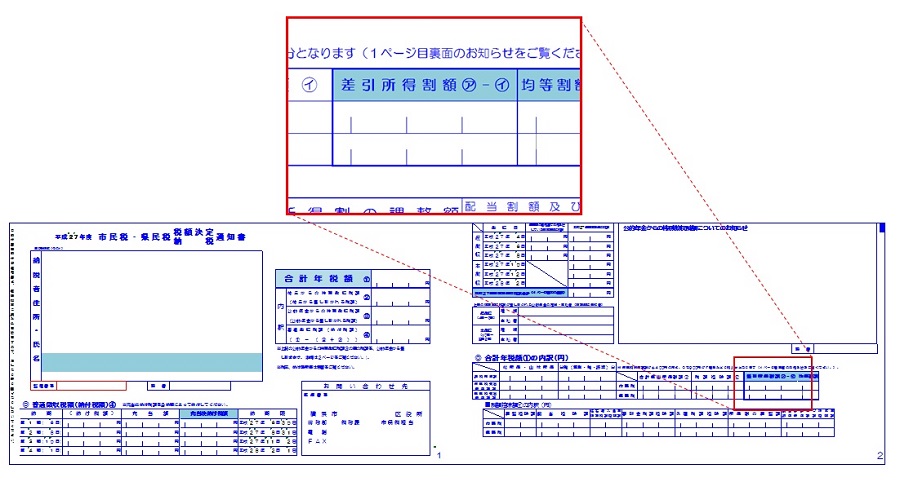

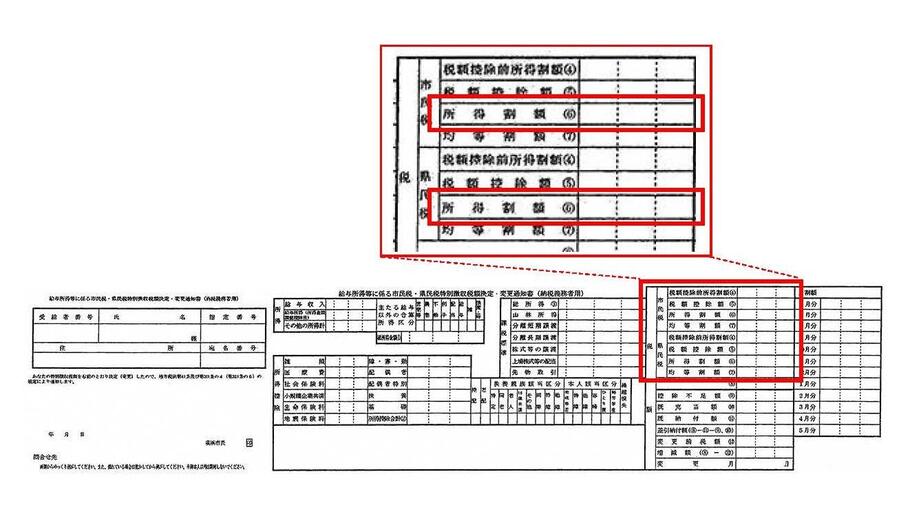

(1)In the case of municipal tax, prefectural tax tax payment letter of advice (normal collection) (we notify in early June every year.)

“Deducted income discount (* 4)” on page 2 “◎ Breakdown of Total Annual Tax Amount (Yen)”

It is style established in Yokohama-shi city tax regulations. The style may be different from other municipalities.

(※4) The limit of the exceptional deduction is 20% of the income percent after the adjustment deduction is applied (10% until 2015).

If there is a tax credit other than the adjustment deduction in the year of the notice you are viewing, the amount of income percent in the frame will be reduced by that amount, so 20% of the stated amount (2015 Until 10%) may not be the special deduction limit.

(2)In the case of municipal tax, prefectural tax special collection tax amount decision letter of advice (special collection) (we notify company of special collection duty person after the middle of May every year.)

"Income percent (* 5)" of municipal tax and prefectural tax in the "tax amount" column

It is stipulated by the Local Tax Law and is common throughout the country.

(※5) The limit of the exceptional deduction is 20% of the income percent after the adjustment deduction is applied (10% until 2015).

If there is a tax credit other than the adjustment deduction in the year of the notice you are viewing, the amount of income percent in the frame will be reduced by that amount, so 20% of the stated amount (2015 Until 10%) may not be the special deduction limit.

About oldness and tax payment one-stop exception system (report exception system)

The hometown tax one-stop exception system (declaration exception system) is the hometown taxpayer when paid income earners who do not need to file a final tax return pay their hometown tax for prefectures and municipalities (subject to special deduction (* 1)) This is a system that allows you to receive donation deductions for hometown tax without having to file a final tax return by applying to the local government (* 2) (for donations after April 1, 2015). 。

If this exception is applied, there will be no deduction (refund) from income tax, and the deduction will be made in the form of a reduction (declaration exception deduction) of personal municipal tax and prefectural tax paid after June of the following year when the hometown tax was paid. Is done.

(※1) Due to the enactment of a law that partially revises the Local Tax Law, etc., a designated system for hometown tax payment was established on June 1, 2019. . As a result, the Minister of Internal Affairs and Communications has designated local organizations that meet the following criteria as hometown tax payment (exceptional deductions) (for the target local organizations, refer to the Ministry of Internal Affairs and Communications website (outside site) Please refer to.) 。

①Local organizations that properly carry out donations

②(A local organization in 1) When sending return goods, a local organization that satisfies all of the following

・The return rate of return items shall be 30% or less.

・Make return goods a local product

This amendment applies to donations paid after June 1, 2019, so donations paid to non-designated organizations after the same day are not subject to special deductions. You.

(※2) Application of exception is necessary to submit oldness and tax payment one-stop exception (report exception) application to each local government that paid oldness and tax when we perform oldness and tax payment.

(※3) If there is a change in the contents of the submitted application, such as a change in Address due to relocation after applying for the application of the exception, please submit registration form to the local government of your hometown taxpayer by January 10 of the year following your hometown tax payment.

◆Notes

(1) Those who fall under the following are not eligible for the Hometown Tax One-Stop Exception System, so in order to receive deductions including income tax, it is necessary to enter and submit a final income tax return as before. (In the following cases, even if you submit your hometown tax payment one-stop (report exception) application to your hometown tax payment local government, it is considered that there was no application for the hometown tax payment one-stop exception system.)

・Those who have paid hometown tax to more than 5 local governments

・Person who submitted municipal tax, prefectural tax return of the year following the year of donation or final income tax return for the year of donation

・Those who are obliged to submit a final income tax return for the year of donation

・Those who have different local governments on January 1 of the year following the donation from Address listed in the special application form for tax return and who have not submitted a notification of the change to their hometown taxpayer by January 10

(2) When we receive donation deduction in person submitting municipal tax, prefectural tax return or final income tax return, we applied for all donation to receive donation deduction in report (application as object of one-stop exception system Please be sure to include your hometown tax payment).

(3) If you file a municipal tax / prefectural tax return or a final tax return after the deadline after the initial tax notification, even if the deduction for the hometown tax one-stop exception was applied in the original notification, the deduction for that amount Since it is considered that there was no deduction, be sure to include all donations that receive donation deductions (including the hometown tax payment applied for as a subject of the one-stop exception system).

◆Calculation method of donation tax credit (when we use oldness and tax payment one-stop exception system)

The sum of the basic deduction + special deduction + declaration exception deduction is the deduction.

●Basic Deductions

Municipal tax…("Total amount of hometown tax payment" or "30% of gross income, etc." -2,000 yen) x 8%

Prefectural tax…("Total amount of hometown tax payment" or "30% of gross income, etc."-2,000 yen) x 2%

●Special deduction (only hometown tax payment applies)

Municipal tax…The lesser of "(Total amount of hometown tax payment-2,000 yen) x deduction ratio (*) x 4/5" or "Municipal tax income percent (after deduction of adjustment deduction) x 20%"

Prefectural tax…The lesser of "(Total amount of hometown tax payment-2,000 yen) x deduction ratio (*) x 1/5" or "Prefectural tax income percent (after deduction of adjustment deduction) x 20%"

●Deduction for tax return (applicable only when using the one-stop exception system)

Municipal tax…"Exceptional deduction (for municipal tax)" calculated above x "Deduction ratio of declaration exception deduction"

Prefectural tax…"Exceptional deduction (for prefectural tax)" calculated above x "Deduction ratio of declaration exception deduction"

| Total amount of difference between taxable gross income (*) and personal deduction from income tax | Deduction ratio |

|---|---|

| 1.95 million yen or less | 5.105/84.895 |

| More than ¥1.95 million and less than ¥3.3 million | 10.21/79.79 |

| More than 3.3 million yen and less than 6.95 million yen | 20.42/69.58 |

| More than 6.95 million yen 9 million yen | 23.483/66.517 |

| Over 9 million yen | 33.693/56.307 |

(※) The taxable gross income amount refers to the taxable gross income amount of municipal tax and prefectural tax.

About the impact on donation tax credit (hometown tax payment) of fixed amount tax reduction in 2024

The fixed amount tax reduction applied in 2024 does not affect the calculation method of donation tax credit. Deduction limit of exception deduction of oldness and tax payment is calculated before fixed amount tax reduction.

Please check here for details on the fixed amount tax cut.

About special tax credit (fixed tax reduction) of individual municipal inhabitant tax and prefectural inhabitant tax for 2024

About hometown tax payment to Yokohama-shi

Please check here.

Thing about oldness and tax payment to Yokohama-shi (we move to page of Policy Bureau financial resources securing promotion section.)

Contact information

If you have any questions, please contact each ward office.

| Ward office | Window | Phone number | E-Mail address |

|---|---|---|---|

| Aoba Ward | 55th floor on the 3rd floor of Aoba Ward Office | 045-978-2241 | ao-zeimu@city.yokohama.lg.jp |

| Asahi Ward | 28th floor, 2nd floor of Asahi Ward Hall Main Building | 045-954-6043 | as-zeimu@city.yokohama.lg.jp |

| Izumi Ward | 304, 3rd floor of Izumi Ward Office | 045-800-2351 | iz-zeimu@city.yokohama.lg.jp |

| Isogo Ward | 34th floor, Isogo Ward Office, 3rd floor | 045-750-2352 | is-zeimu@city.yokohama.lg.jp |

| Kanagawa Ward | 325 on the 3rd floor of Kanagawa Ward Hall Main Building | 045-411-7041 | kg-zeimu@city.yokohama.lg.jp |

| Kanazawa Ward | 304, 3rd floor of Kanazawa Ward Office | 045-788-7744 | kz-zeimu@city.yokohama.lg.jp |

| Konan Ward | 31st floor, Konan Ward Office, 3rd floor | 045-847-8351 | kn-shiminzei@city.yokohama.lg.jp |

| Kohoku Ward | 31st floor, Kohoku Ward Office, 3rd floor | 045-540-2264 | ko-zeimu@city.yokohama.lg.jp |

| Sakae Ward | 30th floor, 3rd floor of Sakae Ward Hall Main Building | 045-894-8350 | sa-zeimu@city.yokohama.lg.jp |

| Seya Ward | 33rd floor, Seya Ward Office, 3rd floor | 045-367-5651 | se-zeimu@city.yokohama.lg.jp |

| Tsuzuki Ward | 34th floor, Tsuzuki Ward Office, 3rd floor | 045-948-2261 | tz-zeimu@city.yokohama.lg.jp |

| Tsurumi Ward | No. 2 on the 4th floor of Tsurumi Ward Office | 045-510-1711 | tr-zeimu@city.yokohama.lg.jp |

| Totsuka Ward | 72th floor, Totsuka Ward Office, 7th floor | 045-866-8351 | to-zeimu@city.yokohama.lg.jp |

| Naka Ward | 43rd floor on the 4th floor of Naka Ward Office Main Building | 045-224-8191 | na-zeimu@city.yokohama.lg.jp |

| Nishi Ward | 44th floor, Nishi Ward Office, 4th floor | 045-320-8341 | ni-zeimu@city.yokohama.lg.jp |

| Hodogaya Ward | 26th floor, 2nd floor of Hodogaya Ward Hall Main Building | 045-334-6241 | ho-zeimu@city.yokohama.lg.jp |

| Midori Ward | 35th floor, Midori Ward Office, 3rd floor | 045-930-2261 | md-zeimu@city.yokohama.lg.jp |

| Minami Ward | 33rd floor, Minami Ward Office, 3rd floor | 045-341-1157 | mn-zeimu@city.yokohama.lg.jp |

Inquiries to this page

Tax Division, Chief Tax Department, Finance Bureau (I cannot answer consultations on individual taxation details and declarations.) Please contact your ward office Tax Division.)

Telephone: 045-671-2253

Telephone: 045-671-2253

Fax: 045-641-2775

Email address: za-kazei@city.yokohama.lg.jp

Page ID: 399-896-158