- Yokohama-shi Top Page

- Living and Procedures

- family register Tax and Insurance

- Taxes

- City tax of Yokohama

- Property tax (land and houses) and city planning tax

- Property tax (land and houses) and city planning tax (details)

- System for calculating the amount of property tax (land) for FY2024

Here's the text.

System for calculating the amount of property tax (land) for FY2024

Last Updated December 19, 2024

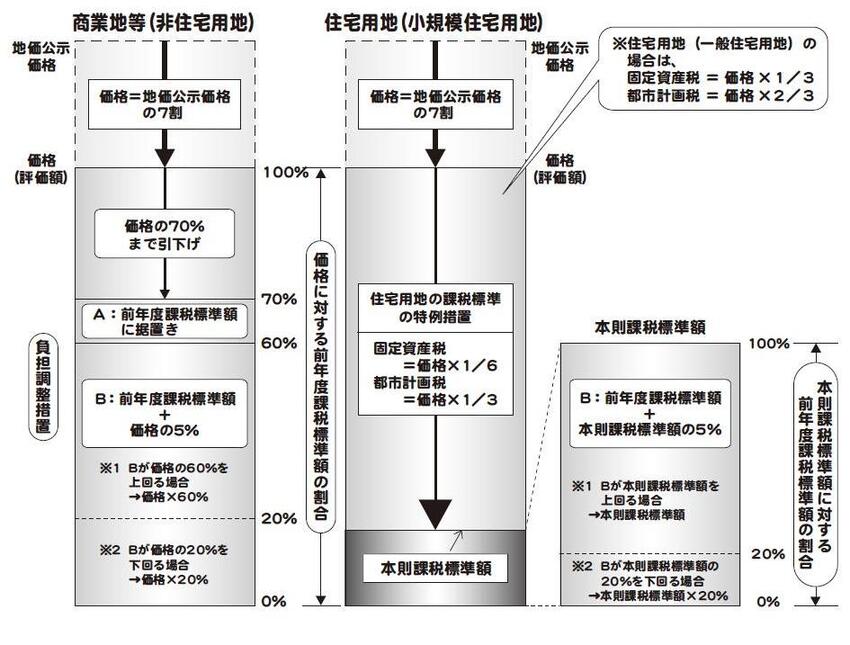

The tax amount of property tax and city planning tax on residential land is determined according to the ratio (burden level) of the previous year's tax standard amount to the price (main rule tax standard amount).

If you specifically show the mechanism of tax calculation, it will be shown below.

Method of calculating the amount of tax on residential land

The tax amount for residential land is calculated according to the following procedure.

(1) Judgment of classification of residential land…We judge which division of small residential land, general residential land or non-residential land corresponds to.

(2) Calculation of burden level…By the following formula, calculate the ratio (burden level) of the previous year's tax standard amount to the price (main rule tax standard amount).

- 2023 standard tax amount / 2024 price (main rule tax standard amount)

(3) Calculation of standard tax amount…Depending on the ratio obtained in (2) for each division of residential land determined in (1), apply to the table listed below, apply the burden adjustment measures, and calculate the standard tax amount for 2024.

(4) Calculation of tax amount…2024 tax amount = 2024 tax standard amount x tax rate (property tax 1.4%, city planning tax 0.3%)

If the tax amount rises as it is when the valuation of the land rises, the burden will increase, so this is a measure to gradually approach the tax burden based on the price (main rule tax standard amount) every year.

In order to balance taxation while preventing the tax amount from significantly changing (up), reduce the tax burden on land with a high burden level (the ratio of the previous year's standard tax amount to the price (main rule tax standard amount)) In addition, for land with a low burden level, the standard tax amount will be raised according to the burden level.

| (1) Classification of residential land | (2) Ratio (burden level) of the previous year's standard tax amount to the price (main rule tax standard amount) | (3) Calculation of standard tax amount (burden adjustment measures) |

|---|---|---|

| Small residential land And general residential land |

More than 100% | Decreased to the standard tax amount of this rule (Note 1) |

| Less than 100% | Previous year's standard tax amount + (main rule tax standard amount x 5%) |

|

| Commercial land, etc. (non-residential land) | More than 70% | Reduced to 70% of the price (Note 2) |

| 60% or more, 70% or less | Deferred to the previous year's standard tax amount | |

| Less than 60% | Previous year's standard tax amount + (price x 5%) |

(Note 1)

In the case of "reduction to the main rule tax standard amount", the method of calculating the 2024 tax standard amount is as follows.

- Property tax

- Small residential land: 2024 standard tax amount = price x 1/6

General residential land: 2024 standard tax amount = price x 1/3 - City planning tax

- Small residential land: 2024 standard tax amount = price x 1/3

General residential land: 2024 standard tax amount = price x 2/3

(Note 2)

In the case of "reduction to 70% of price", the method of calculating the standard tax amount for 2024 is as follows.

2024 standard tax amount (property tax and city planning tax) = price x 70%

Contact information

If you have any questions, please contact each ward office.

| Ward office | Window | Phone number | E-Mail address |

|---|---|---|---|

| Aoba Ward | 51, 3rd floor of Aoba Ward Office | 045-978-2248 | ao-zeimu@city.yokohama.lg.jp |

| Asahi Ward | 29th floor, 2nd floor of Asahi Ward Hall Main Building | 045-954-6047 | as-zeimu@city.yokohama.lg.jp |

| Izumi Ward | 302 on the 3rd floor of Izumi Ward Office | 045-800-2361 | iz-zeimu@city.yokohama.lg.jp |

| Isogo Ward | 36th floor, Isogo Ward Office, 3rd floor | 045-750-2361 | is-zeimu@city.yokohama.lg.jp |

| Kanagawa Ward | 323, 3rd floor of Kanagawa Ward Hall Main Building | 045-411-7053 | kg-zeimu@city.yokohama.lg.jp |

| Kanazawa Ward | 302 on the 3rd floor of Kanazawa Ward Office | 045-788-7749 | kz-zeimu@city.yokohama.lg.jp |

| Konan Ward | 32nd floor, Konan Ward Office, 3rd floor | 045-847-8360 | kn-zeimu@city.yokohama.lg.jp |

| Kohoku Ward | 35th floor, Kohoku Ward Office, 3rd floor | 045-540-2275 | ko-zeimu@city.yokohama.lg.jp |

| Sakae Ward | 32nd floor, 3rd floor of Sakae Ward Hall Main Building | 045-894-8361 | sa-zeimu@city.yokohama.lg.jp |

| Seya Ward | 31st floor, Seya Ward Office, 3rd floor | 045-367-5661 | se-zeimu@city.yokohama.lg.jp |

| Tsuzuki Ward | 32nd floor, Tsuzuki Ward Office, 3rd floor | 045-948-2265 | tz-zeimu@city.yokohama.lg.jp |

| Tsurumi Ward | 5th floor on the 4th floor of Tsurumi Ward Office | 045-510-1727 | tr-zeimu@city.yokohama.lg.jp |

| Totsuka Ward | 73rd floor, Totsuka Ward Office, 7th floor | 045-866-8361 | to-zeimu@city.yokohama.lg.jp |

| Naka Ward | 45th floor, 4th floor of Naka Ward Office Main Building | 045-224-8201 | na-zeimu@city.yokohama.lg.jp |

| Nishi Ward | 43rd floor, Nishi Ward Office, 4th floor | 045-320-8349 | ni-zeimu@city.yokohama.lg.jp |

| Hodogaya Ward | 28th floor, 2nd floor of Hodogaya Ward Hall Main Building | 045-334-6250 | ho-zeimu@city.yokohama.lg.jp |

| Midori Ward | 34th floor, Midori Ward Office, 3rd floor | 045-930-2268 | md-zeimu@city.yokohama.lg.jp |

| Minami Ward | 31st floor, Minami Ward Office, 3rd floor | 045-341-1161 | mn-zeimu@city.yokohama.lg.jp |

Inquiries to this page

Property Tax Division, Chief Tax Department, Finance Bureau Land Section

Telephone: 045-671-2258

Telephone: 045-671-2258

Fax: 045-641-2775

Email address: za-koteishisanzei@city.yokohama.lg.jp

Page ID: 994-304-196