Here's the text.

How to determine the price of fixed assets

Last Updated December 19, 2024

The price of fixed assets is evaluated based on the "Fixed Asset Valuation Standards" established by the Minister of Internal Affairs and Communications, and the mayor determines the price and registers it in the fixed asset tax book.

The price of land and houses is to be reviewed every three years, and this is called revaluation. Fiscal 2024 is the year of revaluation.

As a general rule, the price of land and houses will be deferred in the following fiscal year and the next two years after the revaluation year. However, for land, exceptions are made only when there is a conversion of land or a joint brush, or when the land price has declined significantly, or when the house has been renovated or partially demolished. Review the price.

Regarding the evaluation of depreciable assets, which are business assets, the status as of January 1 of each year must be declared by January 31, and the price will be calculated every year based on that. .

The price of land is calculated based on the normal trading price calculated based on the actual trading value based on the "Fixed Asset Valuation Standards". However, with regard to the prices of residential land and land equivalent to residential land, since the revaluation in fiscal 1994, the evaluation has been balanced and optimized with a target of 70% of the published land price, and even in the revaluation in fiscal 2024, We continue to promote the balance and appropriateness of evaluation.

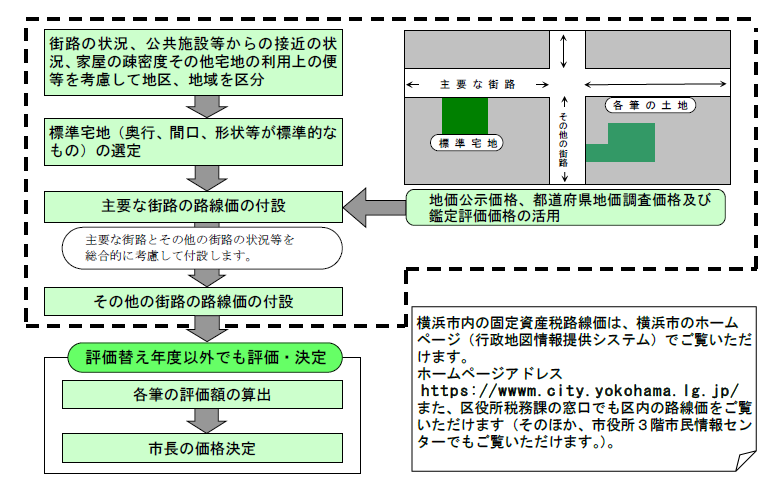

Evaluation method of residential land

The valuation of the house is to be performed based on the rebuilding price in the "Fixed Asset Valuation Standards".

This is based on the construction cost (reconstruction price) required when a new house similar to the house to be evaluated is newly built, multiplied by the depreciation rate (aging deduction correction rate) according to the number of years elapsed since the new construction It is a method to determine the price.

The details of how to calculate the price are as follows.

- Evaluation of new extension houses

In the case of a new extension house, on-site surveys of the status of materials and equipment used for roofs, outer walls, interiors of each room, etc. (Note 1), and apply the unit price specified in the “Fixed Asset Valuation Standards” for those materials. See the rebuilding price. The calculated rebuilding price is calculated by multiplying the calculated rebuilding price by the depreciation rate over one year (aging deduction correction rate) (Note 2).

(Note 1) Investigators (the ward office Tax Division house staff) visit and ask for a field survey of the house.

(Note 2) New houses are taxed from the year following the year of new construction.

- Houses other than new extensions (existing houses)

Houses other than the new extension will be reviewed in the year of revaluation every three years. The price after the review is the correction rate determined in consideration of trends in building prices for three years (referred to as the rebuilding cost rating correction rate. In the revaluation in 2024, wooden houses 1.11 and non-wooden houses 1.07 according to the fixed asset valuation standard) ) To calculate the rebuilding price newly, and multiply the rebuilding value obtained by multiplying the rebuilding value obtained from the age of the correction. After that, compare the price after the review with the price before the review to determine the lower price.

Newly built or renovated houses are subject to property tax and city planning tax from the year following completion.

In order to calculate the valuation that forms the basis of these tax amounts, an investigator (the ward office Tax Division house staff) visits and investigates the house based on the Local Tax Law.

Specifically, we will investigate the status of roofs and outer walls, interiors of each room, building equipment, etc.

When visiting the survey, we will contact you in advance and adjust the schedule of the survey, so we ask for your understanding and cooperation.

In addition, investigator carries "tax collection officer card" and "fixed asset evaluation assistant card" at the time of investigation.

(Measures against the spread of COVID-19)

To prevent COVID-19 infections, investigators wear masks during the survey.

Contact information

If you have any questions, please contact each ward office.

| Ward office | Land Section window number Phone number | House contact number Phone number | E-Mail address |

|---|---|---|---|

| Aoba Ward | 51, 3rd floor of Aoba Ward Office 045-978-2248 | 50th floor on the 3rd floor of Aoba Ward Office 045-978-2254 | ao-zeimu@city.yokohama.lg.jp |

| Asahi Ward | 29th floor, 2nd floor of Asahi Ward Hall Main Building 045-954-6047 | 29th floor, 2nd floor of Asahi Ward Hall Main Building 045-954-6053 | as-zeimu@city.yokohama.lg.jp |

| Izumi Ward | 302 on the 3rd floor of Izumi Ward Office 045-800-2361 | 302 on the 3rd floor of Izumi Ward Office 045-800-2365 | iz-zeimu@city.yokohama.lg.jp |

| Isogo Ward | 36th floor, Isogo Ward Office, 3rd floor 045-750-2361 | 36th floor, Isogo Ward Office, 3rd floor 045-750-2365 | is-zeimu@city.yokohama.lg.jp |

| Kanagawa Ward | 323, 3rd floor of Kanagawa Ward Hall Main Building 045-411-7053 | 322, 3rd floor of Kanagawa Ward Hall Main Building 045-411-7054 | kg-zeimu@city.yokohama.lg.jp |

| Kanazawa Ward | 302 on the 3rd floor of Kanazawa Ward Office 045-788-7749 | 301 on the 3rd floor of Kanazawa Ward Office 045-788-7754 | kz-zeimu@city.yokohama.lg.jp |

| Konan Ward | 32nd floor, Konan Ward Office, 3rd floor 045-847-8360 | 32nd floor, Konan Ward Office, 3rd floor 045-847-8365 | kn-zeimu@city.yokohama.lg.jp |

| Kohoku Ward | 35th floor, Kohoku Ward Office, 3rd floor 045-540-2275 | 34th floor, Kohoku Ward Office, 3rd floor 045-540-2281 | ko-zeimu@city.yokohama.lg.jp |

| Sakae Ward | 32nd floor, 3rd floor of Sakae Ward Hall Main Building 045-894-8361 | 33rd floor, 3rd floor of Sakae Ward Hall Main Building 045-894-8365 | sa-zeimu@city.yokohama.lg.jp |

| Seya Ward | 31st floor, Seya Ward Office, 3rd floor 045-367-5661 | 31st floor, Seya Ward Office, 3rd floor 045-367-5665 | se-zeimu@city.yokohama.lg.jp |

| Tsuzuki Ward | 32nd floor, Tsuzuki Ward Office, 3rd floor 045-948-2265 | 33rd floor, Tsuzuki Ward Office, 3rd floor 045-948-2271 | tz-zeimu@city.yokohama.lg.jp |

| Tsurumi Ward | 5th floor on the 4th floor of Tsurumi Ward Office 045-510-1727 | 4th floor, 6th floor, Tsurumi Ward Office 045-510-1730 | tr-zeimu@city.yokohama.lg.jp |

| Totsuka Ward | 73rd floor, Totsuka Ward Office, 7th floor 045-866-8361 | 73rd floor, Totsuka Ward Office, 7th floor 045-866-8368 | to-zeimu@city.yokohama.lg.jp |

| Naka Ward | 45th floor, 4th floor of Naka Ward Office Main Building 045-224-8201 | 44th floor, Naka Ward Office Main Building, 4th floor 045-224-8204 | na-zeimu@city.yokohama.lg.jp |

| Nishi Ward | 43rd floor, Nishi Ward Office, 4th floor 045-320-8349 | 43rd floor, Nishi Ward Office, 4th floor 045-320-8354 | ni-zeimu@city.yokohama.lg.jp |

| Hodogaya Ward | 28th floor, 2nd floor of Hodogaya Ward Hall Main Building 045-334-6250 | 28th floor, 2nd floor of Hodogaya Ward Hall Main Building 045-334-6254 | ho-zeimu@city.yokohama.lg.jp |

| Midori Ward | 34th floor, Midori Ward Office, 3rd floor 045-930-2268 | 34th floor, Midori Ward Office, 3rd floor 045-930-2274 | md-zeimu@city.yokohama.lg.jp |

| Minami Ward | 31st floor, Minami Ward Office, 3rd floor 045-341-1161 | 31st floor, Minami Ward Office, 3rd floor 045-341-1163 | mn-zeimu@city.yokohama.lg.jp |

Inquiries to this page

Property Tax Division, Chief Tax Department, Finance Bureau Land Section

Telephone: 045-671-2258

Telephone: 045-671-2258

Fax: 045-641-2775

Email address: za-koteishisanzei@city.yokohama.lg.jp

Property Tax Division, Property Tax Division, Finance Bureau

Telephone: 045-671-2260

Telephone: 045-671-2260

Fax: 045-641-2775

Email address: za-koteishisanzei@city.yokohama.lg.jp

Page ID: 769-403-672