- Yokohama-shi Top Page

- Living and Procedures

- family register Tax and Insurance

- Taxes

- City tax of Yokohama

- Individual municipal tax and prefectural tax

- About tax system revision about personal residence tax

- Notice of Revision of Resident Tax System for FY2014

Here's the text.

Notice of Revision of Resident Tax System for FY2014

Last Updated January 16, 2024

The contents of the tax system revision of personal residence tax implemented from 2014 are as follows.

![]() About increase of per capita rate

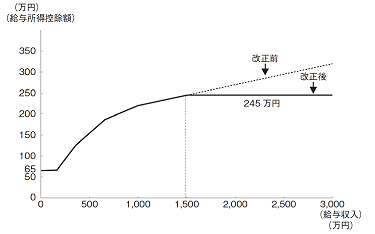

About increase of per capita rate![]() Revision of employment income deduction

Revision of employment income deduction![]() About review of donation tax credit to affect oldness and donation

About review of donation tax credit to affect oldness and donation

(1) Extension of Yokohama green tax to work on green conservation creation

It is an urgent task to pass on the green city of Yokohama to the next generation. Also, once green is lost, it is difficult to regain it. For this reason, as an important financial source of the "Yokohama Green Up Plan", which protects, creates and nurtures greenery, the "Yokohama Green Tax" (900 yen per year on per capita rate), please continue to bear the burden for 5 years from 2014 to 2018.

(2) Increase the per capita rate of personal municipal tax and prefectural tax for earthquake disaster countermeasures business

In Yokohama City and Kanagawa Prefecture, in order to secure financial resources such as earthquake disaster countermeasures projects, with the enforcement of the extraordinary special law of the Local Tax Law, temporary personal municipal tax and prefectural tax for 10 years from 2014 to 2023 We raised the per capita rate of tax by 500 yen each.

Thank you for your understanding and cooperation.

| Current per capita rate | Amount raised | Per capita rate after raising | |

|---|---|---|---|

| Municipal tax | 3,900 yen ※1 | 500 yen | 4,400 yen |

| Prefectural tax | 1,300 yen ※2 | 500 yen | 1,800 yen |

| Total | 5,200 yen | 1,000 yen | 6,200 yen |

※1 In Yokohama City, the excess tax "Yokohama Green Tax" is implemented, so 900 yen is added.

※2 In Kanagawa Prefecture, the excess tax “Water Source Environmental Conservation Tax” is implemented, so an additional 300 yen is added.

(1) An upper limit of 2.45 million yen has been set for the deduction of employment income when the amount of income such as salary exceeds 15 million yen. (If a salary income of more than 15 million yen, it will be 2.45 million yen.)

(2) Regarding specific expenditure deductions, qualifications for lawyers, certified public accountants, tax accountants, etc., which are directly required for performing their duties, and work expenses (up to 650,000 yen) required for their duties, such as book expenses, clothing expenses, and entertainment expenses required for their duties have been added. Was.

(3) If the total amount of specific expenditures for that year exceeds the amount specified below, the excess amount can be added to the employment income deduction.

Oh, when the amount of income such as salary during the year is less than 15 million yen ... An amount equivalent to one half of the deduction of salary income during the year

B. If the amount of income such as salary during the year is more than 15 million yen ... 1.25 million yen

With the special income tax for reconstruction being imposed from 2013, for the 25 years from 2014 to 2038, the marginal tax rate of the income tax used to calculate the special deduction for donation tax credit will be calculated by adding the rate obtained by multiplying by (2.1%).

| Basic Deductions | Municipal tax: (Donation amount -2,000 yen) x 6% Prefectural tax: (Donation amount -2,000 yen) x 4% |

|---|---|

| Special deductions | Municipal tax: (donation amount-2,000 yen) x (90%-margin tax rate of income tax 0-40%) x 3/5 Prefectural tax: (donation amount-2,000 yen) x (90%-margin tax rate of income tax 0-40%) x 2/5 ※The exceptional deduction is limited to 10% of the income percent. |

| Basic Deductions | Municipal tax: (Donation amount -2,000 yen) x 6% Prefectural tax: (Donation amount -2,000 yen) x 4% |

|---|---|

| Special deductions | Municipal tax: (donation amount-2,000 yen) x (90%-margin tax rate of income tax 0-40% x 1.021) x 3/5 Prefectural tax: (donation amount-2,000 yen) x (90%-margin tax rate of income tax 0-40% x 1.021) x 2/5 ※The exceptional deduction is limited to 10% of the income percent. |

Inquiries to this page

Tax Division, Chief Tax Department, Finance Bureau

Telephone: 045-671-2253

Telephone: 045-671-2253

Fax: 045-641-2775

Email address: za-kazei@city.yokohama.lg.jp

Page ID: 608-830-601