- Yokohama-shi Top Page

- Living and Procedures

- family register Tax and Insurance

- Taxes

- City tax of Yokohama

- Individual municipal tax and prefectural tax

- About tax system revision about personal residence tax

- Notification of revision of residence tax tax system (for fiscal 2021)

Here's the text.

Notification of revision of residence tax tax system (for fiscal 2021)

Last Updated December 3, 2024

The contents of the tax system revision of personal municipal tax and prefectural tax that will be implemented from 2021 are as follows.

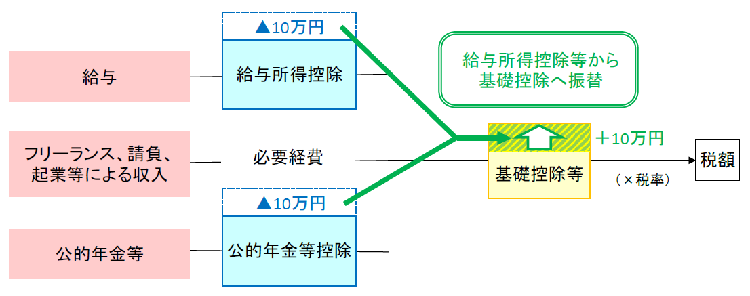

■Reduction of employment income deductions and public pension deductions, and increase of basic deductions

□Revision of employment income deduction

□Revision of public pension deductions

□Review of Basic Deductions

■Creation of income adjustment deductions

■Review of tax measures for unmarried single parents and widows (widows) deductions

■Review of Special Deductions for Blue Declaration

■Review of special provisions for calculating income such as business income of domestic workers

■Review of income amount requirements such as income deductions

■Review of spouse's income category in special spouse deductions

■Revision of adjustment deduction

■Revision of the difference in personal deductions

■Review of tax exemption standards for residence tax

■Tax measures for emergency economic measures against COVID-19 infection

□Flexibility of application requirements for mortgage deduction

□Application of donation deduction to spectators who have waived the right to request refund for organizers who have canceled cultural arts and sports events, etc.

Based on the diversification of work styles, from the viewpoint of supporting work style reforms, the deduction of employment income deductions and deductions for public pensions, etc., applicable only to specific income has been reduced by 100,000 yen, and any income The deduction for basic deductions applied to will be raised by 100,000 yen (income tax: 480,000 yen, personal residence tax: 430 yen).

※ For those who have both earned income and pension income, only one deduction will be reduced.

Regarding employment income deductions, which have been pointed out to be excessive compared to work-related expenses and levels in other countries, the following review was conducted based on the policy of `` gradually optimizing deductions to major countries '' Was.

- The employment income deduction has been reduced by 100,000 yen.

- The salary income to which the upper limit of the employment income deduction is applied has been reduced to 8.5 million yen, and the upper limit has been reduced to 1.95 million yen.

In addition, an income adjustment deduction (described later) will be newly established so that there is no burden on child-rearing households and nursing care households.

| Salary income (A) | Deduction of employment income | |

|---|---|---|

| (After revision) | (before revision) | |

| 1,625,000 yen or less | 550,000 yen | 650,000 yen |

| More than 1,625,000 yen 1,800,000 yen or less | A×40% -100,000 yen | A×40% |

| More than 1.8 million yen and less than 3.6 million yen | A × 30% +80,000 yen | A×30% +180,000 yen |

| More than 3.6 million yen and less than 6.6 million yen | A × 20% +440,000 yen | A × 20% +540,000 yen |

| More than 6.6 million yen 8.5 million yen or less | A × 10% + 1,100,000 yen | A × 10% + 1,200,000 yen |

| More than 8.5 million yen 10 million yen or less | 1,950,000 yen | |

| More than 10 million yen | 2,200,000 yen | |

※If the amount of income such as salary is less than 6.6 million yen, salary income will be calculated according to Appendix 5 of the Income Tax Law, regardless of the table above.

It has been pointed out that public pension deductions, unlike employment income deductions, have no upper limit on deductions and are generous to high-income pension income earners. Based on these points, the following review was conducted from the viewpoint of ensuring fairness within and between generations.

- The amount of public pension deductions will be reduced by 100,000 yen.

- If the amount of income from public pension, etc. exceeds 10 million yen, the maximum deduction for public pensions is 1,955,000 yen.

- If the total amount of income other than miscellaneous income related to public pension, etc. exceeds 10 million yen, the public pension deduction will be reduced.

| Public pension, etc. (A) | (After revision) | (before revision) | |||||

|---|---|---|---|---|---|---|---|

| Total income related to income other than miscellaneous income related to public pension, etc. | |||||||

| More than 20 million yen | More than 10 million yen | 10 million yen or less | |||||

| 65 years old Less than | Less than 1.3 million yen | 400,000 yen | 500,000 yen | 600,000 yen | 700,000 yen | ||

| 1.3 million yen or more Less than 4.1 million yen | A×25% +75,000 yen | A×25% +175,000 yen | A×25% +275,000 yen | A×25% +375,000 yen | |||

| 65 years old Above | Less than 3.3 million yen | 900,000 yen | 1 million yen | 1.1 million yen | 1.2 million yen | ||

| 3.3 million yen or more Less than 4.1 million yen | A×25% +75,000 yen | A×25% +175,000 yen | A×25% +275,000 yen | A×25% +375,000 yen | |||

| 4.1 million yen or more Less than 7.7 million yen | A×15% +485,000 yen | A×15% +585,000 yen | A×15% +685,000 yen | A×15% +785,000 yen | |||

| 7.7 million yen or more Less than 10 million yen | A×5% +1,255,000 yen | A×5% +1,355,000 yen | A×5% +1,455,000 yen | A×5% +1,555,000 yen | |||

| 10 million yen or more | 1,755,000 yen | 1,855,000 yen | 1,955,000 yen | ||||

| Public pension, etc. (A) | (After revision) | (before revision) | |||||

|---|---|---|---|---|---|---|---|

| Total income related to income other than miscellaneous income related to public pension, etc. | |||||||

| More than 20 million yen | More than 10 million yen | 10 million yen or less | |||||

| 65 years old Less than | Less than 1.3 million yen | A to 400,000 yen | A to 500,000 yen | A to 600,000 yen | A to 700,000 yen | ||

| 1.3 million yen or more Less than 4.1 million yen | A×75% -75,000 yen | A×75% -175,000 yen | A×75% -275,000 yen | A×75% -375,000 yen | |||

| 65 years old Above | Less than 3.3 million yen | A to 900,000 yen | A to 1 million yen | A to 1.1 million yen | A to 1.2 million yen | ||

| 3.3 million yen or more Less than 4.1 million yen | A×75% -75,000 yen | A×75% -175,000 yen | A×75% -275,000 yen | A×75% -375,000 yen | |||

| 4.1 million yen or more Less than 7.7 million yen | A×85% -485,000 yen | A×85% -585,000 yen | A×85% -685,000 yen | A×85% -785,000 yen | |||

| 7.7 million yen or more Less than 10 million yen | A×95% -1,255,000 yen | A×95% -1,355,000 yen | A×95% -1,455,000 yen | A×95% -1,555,000 yen | |||

| 10 million yen or more | A-1,755,000 yen | A-1,855,000 yen | A-1,955,000 yen | ||||

Basic deductions were reviewed as follows from the viewpoint of supporting work style reforms and points out the necessity of reducing the tax burden on high-income earners.

- The basic deduction will be raised by 100,000 yen.

- For taxpayers whose total income exceeds 24 million yen, basic deductions will gradually decrease according to the total income amount, and basic deductions will not be applied to taxpayers whose total income amount exceeds 25 million yen. Will not be

| Total income | Resident tax | Income tax | ||||

|---|---|---|---|---|---|---|

| (After revision) | (before revision) | (After revision) | (before revision) | |||

| 24 million yen or less | 430,000 yen | 330,000 yen | 480,000 yen | 380,000 yen | ||

Over 24 million yen 24.5 million yen or less | 290,000 yen | 320,000 yen | ||||

Over 24.5 million yen 25 million yen or less | 150,000 yen | 160,000 yen | ||||

| Over 25 million yen | No applicable | No applicable | ||||

The employment income deduction was reviewed, and the employment income deduction when the salary income exceeded 8.5 million yen was reduced, but for those who have burdens such as child care and nursing care, measures were taken not to increase the burden. Was.

In addition, for those who have both employment income and pension income, both the employment income deduction and the public pension deduction will be reduced by 100,000 yen, so measures have been taken to prevent the burden from increasing.

In the case of 1 and 2, the deduction for income adjustment will be deducted from employment income.

1. When the amount of salary income exceeds 8.5 million yen and falls under any of the following (1) to (3)

(1) The taxpayer is a person with special disability

(2) Have dependent relatives under the age of 23

(3) Have the same living spouse or dependent relative who is a special disabled person

※ (2)For dependent relatives of (3) and spouses of the same livelihood (hereinafter referred to as dependent relatives, etc.), income adjustment deductions can be applied even if the dependent relatives are subject to dependent deductions of others. I can do it. However, full-time employees are not eligible.

[Computational formula]

Income adjustment deduction = (income such as salary (*)-8.5 million yen) x 10%

(※) If the amount of salary income exceeds 10 million yen, 10 million yen will be deducted from salary income, so a maximum of 150,000 yen will be deducted from salary income.

2. If there are both salary income and miscellaneous income related to public pension, etc., and the total amount of that amount exceeds 100,000 yen

[Computational formula]

Income adjustment deduction = (salary income + miscellaneous income related to public pension, etc.) -100,000 yen

※ A maximum of 100,000 yen will be deducted from your salary income.

If both 1 and 2 apply, 2 will be deducted from the employment income amount after deduction of 1.

<Example of calculation of income adjustment deduction>

1. If your salary income is 9.5 million yen and you support a 10-year-old child

Income adjustment deduction 100,000 yen = (9.5 million yen-8.5 million yen) x 10%

2. When salary income is 630,000 yen and public pension income is 1.3 million yen (age 68 years old)

Amount after deduction of employment income (A') 80,000 yen = 630,000 yen-Salary income deduction 550,000 yen

Amount of miscellaneous income related to public pension, etc. (B") 200,000 yen = 1.3 million yen - Deductions for public pensions 1.1 million yen

→(B") exceeds 100,000 yen, so it will be 100,000 yen.

Income adjustment deduction 80,000 yen = (A') 80,000 yen + (B') 100,000 yen to 100,000 yen

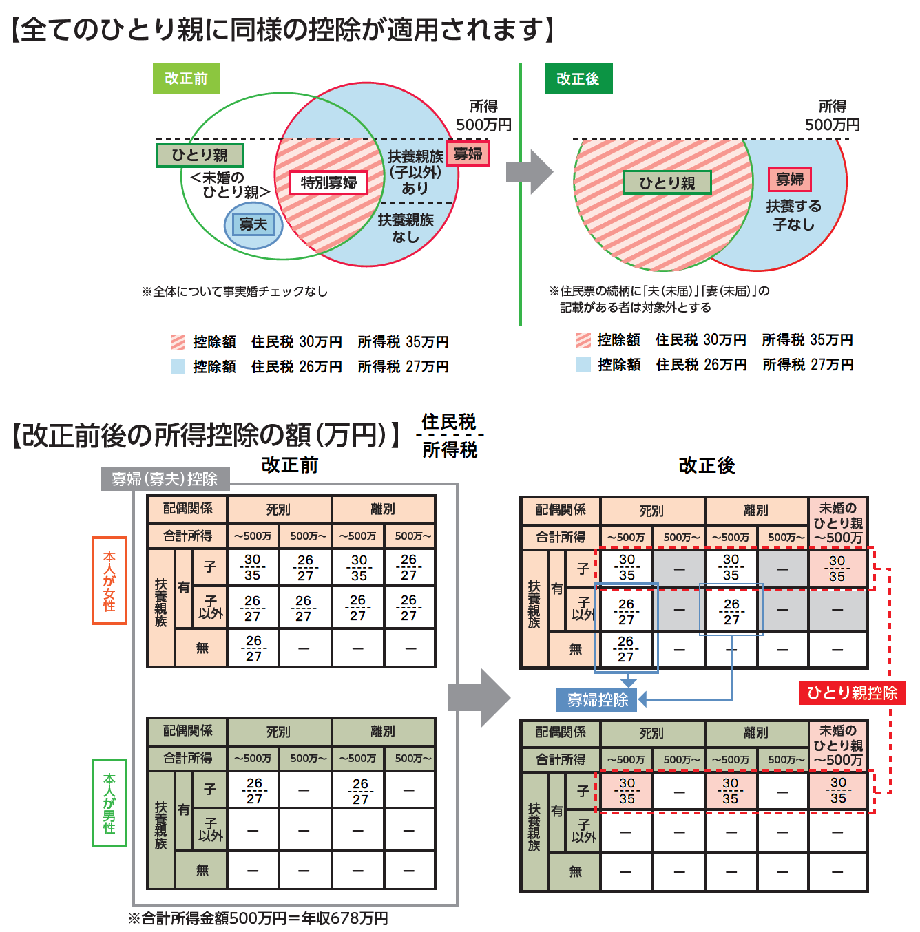

From the viewpoint of realizing a fair tax system for all single-parent families, in order to simultaneously eliminate "inequity due to marriage history" and "inequity between male single parents and female single parents" , The following review was conducted.

1. About single-parent deduction

Regardless of marriage history or gender, a child who has the same livelihood (except those who are considered to be the same living spouse or dependent relative of another person, the total amount of gross income etc. is 480,000 yen or less) For single persons, "single parent deduction" (deduction of 300,000 yen) will be applied.

※ The tax reform in fiscal 2019 (tax exemption for unmarried single parents) was revised in fiscal 2020, and single-parent deductions are no longer limited to Child Raising Allowance recipients (fathers or mothers of elementary school student under the age of 18).

2. Review of widow deductions

For widows other than the above, the deduction of 260,000 yen will continue to be applied as a widow deduction, and widows with dependent relatives other than children will also be subject to income restrictions (total income of 5 million yen or less). Was.

※ For both single-parent deductions and widow deductions, those who have a "husband (not notified)" or "wife (not notified)" in the relationship of resident certificate are not eligible.

As the minimum guarantee for employment income deduction is reduced from 650,000 yen to 550,000 yen, the deduction for blue tax return special deduction for those who record the contents of the transaction in accordance with the principle of regular bookkeeping will be reduced to 550,000 yen (before revision: 650,000 yen).

In addition to the previous requirements for the special blue tax return deduction, it has been decided that if the following requirements are met, a special blue tax return deduction of 650,000 yen will be received.

- Submit a final income tax return, balance sheet, profit and loss statement, etc. using e-Tax by the deadline.

- Provision and preservation of statutory electromagnetic records for journals and general ledgers.

※ There is no revision of the special deduction for blue tax return of 100,000 yen, so it will be the same as before.

Special deduction for blue tax return (move to the NTA website) (External site)

Regarding the calculation of the business income or miscellaneous income of persons who continuously provide human services to specific persons such as domestic workers, diplomats, collectors, etc. (houseworkers, etc.) If the necessary expenses to be deducted from the total income amount in calculating the amount of income is less than the minimum guarantee of employment income deduction, the actual minimum deduction is required from the viewpoint of balancing the domestic workers and the part-time employees. Even if the necessary expenses are deducted from the amount is deducted.

As the minimum guarantee for employment income deduction is reduced from 650,000 yen to 550,000 yen, the minimum guarantee amount to be included in the necessary expenses for domestic workers etc. will be reduced to 550,000 yen (before revision: 650,000 yen). It was decided.

Along with the revision of basic deductions and employment income deductions, it has been decided to raise 100,000 yen each for the amount standard that determines the range of the following persons, which was set based on those deductions.

1. Same living spouse and dependent relatives

Those whose total income is less than 480,000 yen (before revision: 380,000 yen)

2. Working Students

A person whose total income is 750,000 yen or less (before revision: 650,000 yen) or less, and whose total income pertaining to income other than employment income is 100,000 yen or less

With the revision of the amount standard that determines the range of spouses with the same livelihood, the spouse's income category in special spouse deductions will be increased by 100,000 yen each.

| Total income of taxpayers⇨ | 9 million yen or less | Over 9 million yen | Over 9.5 million yen | ||||

|---|---|---|---|---|---|---|---|

| Total spouse’s income⇩ | Resident tax | Income tax | Resident tax | Income tax | Resident tax | Income tax | |

| (After revision) | (before revision) | ||||||

Over 480,000 yen 950,000 yen or less | Over 380,000 yen 850,000 yen or less | 330,000 yen | 380,000 yen | 220,000 yen | 260,000 yen | 110,000 yen | 130,000 yen |

Over 950,000 yen 1,000,000 yen or less | Over 850,000 yen 900,000 yen or less | 330,000 yen | 360,000 yen | 220,000 yen | 240,000 yen | 120,000 yen | |

Over 1 million yen 1.05 million yen or less | Over 900,000 yen 950,000 yen or less | 310,000 yen | 210,000 yen | 110,000 yen | |||

Over 1.05 million yen 1.1 million yen or less | Over 950,000 yen 1,000,000 yen or less | 260,000 yen | 180,000 yen | 90,000 yen | |||

Over 1.1 million yen 1.15 million yen or less | Over 1 million yen 1.05 million yen or less | 210,000 yen | 140,000 yen | 70,000 yen | |||

Over 1.15 million yen 1.2 million yen or less | Over 1.05 million yen 1.1 million yen or less | 160,000 yen | 110,000 yen | 60,000 yen | |||

Over 1.2 million yen 1.25 million yen or less | Over 1.1 million yen 1.15 million yen or less | 110,000 yen | 80,000 yen | 40,000 yen | |||

Over 1.25 million yen 1.3 million yen or less | Over 1.15 million yen 1.2 million yen or less | 60,000 yen | 40,000 yen | 20,000 yen | |||

Over 1.3 million yen 1.33 million yen or less | Over 1.2 million yen 1.23 million yen or less | 30,000 yen | 20,000 yen | 10,000 yen | |||

With the review of the basic deduction, residents' tax adjustment deduction has no longer been applied to taxpayers whose total income exceeds 25 million yen.

※ For details on adjustment deductions, see Tax Credits.

The following review has been made regarding the difference between personal deductions used for calculating adjustment deductions and donation tax credits (hometown tax payment).

- There is no basic deduction or adjustment deduction for taxpayers whose total income exceeds 25 million yen, but there is a difference in the personal deduction of 50,000 yen for basic deduction when calculating donation tax credit. It is assumed.

- For taxpayers whose total income is more than 24 million yen and less than 25 million yen, the difference between the personal deduction of basic deduction is the actual deduction (total income is more than 24 million yen and 24.5 million yen or less Resident tax: 290,000 yen / income tax: 320,000 yen, regardless of 24.5 million yen or less Resident tax: 15 million yen / 15 million yen / 15 million yen / 5 million yen / income tax:

- Regarding the difference in the personal deduction of the father's single-parent deduction, it was 10,000 yen regardless of the actual deduction (resident tax: 300,000 yen, income tax: 350,000 yen).

With the revision of employment income deductions, deductions for public pensions, and basic deductions, the amount of tax exemption for residence tax has been increased by 100,000 yen each as follows.

(1) Persons who are exempt from tax on both per capita and income rates

Persons with disabilities, minors, widows or single-parents whose total income in the previous year was less than 1.35 million yen (before revision: 1.25 million yen)

(2) Person who is exempt from per capita rate

People without dependents…Persons whose total income in the previous year was less than 350,000 yen + 100,000 yen

A person with a dependent…Persons whose total income in the previous year is less than "350,000 yen x (person + spouse of the same livelihood + number of dependent relatives) + 210,000 yen + 100,000 yen"

(3) Those who are exempt from income tax

People without dependents…Persons whose total income, etc. in the previous year was 350,000 yen + 100,000 yen or less

A person with a dependent…Persons whose gross income, etc. in the previous year is less than "350,000 yen x (person + spouse of the same livelihood + number of dependent relatives) + 320,000 yen + 100,000 yen"

※ (2)In (3), the bold part is the revised part.

※ Since deductions for employment income and deductions for public pensions have been reduced by 100,000 yen each, the amount of tax-exempt income and income from public pension and others has been the same as before the revision.

1. Regarding the special measures for the deduction period of the mortgage tax reduction for 13 years, even if the occupancy is delayed due to the impact of COVID-19 infection (December 31, 2020), if all of the following requirements are met, it will be subject to the special measures.

Requirements required to receive special measures

(1)Please move in by December 31, 2021.

(2)The contract must be made by a certain date.

・When building a new custom house: end of September, 2020

・When acquiring a condominium or existing house, or when expanding or renovating: end of November, 2020

(3)Due to the impact of COVID-19, occupancy of custom-built homes, condominiums, existing homes, or homes that have been renovated has been delayed.

2. Regarding the occupancy deadline requirement for mortgage tax reduction when acquiring an existing house (within 6 months from the date of acquisition), even if the extension or renovation work performed after the acquisition is delayed due to the effects of COVID-19 infection, If all of the requirements are met, the occupancy deadline will be "within 6 months from the date of completion of extension / remodeling, etc."

Requirements required to receive special measures for occupancy deadlines

(1) You must move in within 6 months from the date of completion of extension or remodeling.

(2) Contracts for extension or renovation have been made by one of the following dates.

・Up to 5 months after the date of acquisition of existing housing

・From the date of enforcement of the relevant tax bill (April 30, 2020) to two months after (even if the contract is made before the date of enforcement)

(3) Due to the impact of COVID-19 infection, the move into the house after the renovation, etc., was delayed due to the extension or renovation of the acquired existing house.

In order to support the movement of support for cultural arts and sports activities amid the spread of COVID-19, special measures have been set up to reduce the tax burden similar to other donation deductions if an individual who purchases tickets etc. declines to receive a refund for events designated by the Minister of Education, Culture, Sports, Science and Technology.

If you donate to the organizer of the event without receiving a refund of tickets, etc., you will receive income tax (select either income deduction or tax deduction) for such refund amount (up to 200,000 yen per year). You can receive tax incentives for residence tax (donation tax credit).

Contact information

If you have any questions, please contact each ward office.

| Ward office | Window | Phone number | E-Mail address |

|---|---|---|---|

| Aoba Ward | 55th floor on the 3rd floor of Aoba Ward Office | 045-978-2241 | ao-zeimu@city.yokohama.lg.jp |

| Asahi Ward | 28th floor, 2nd floor of Asahi Ward Hall Main Building | 045-954-6043 | as-zeimu@city.yokohama.lg.jp |

| Izumi Ward | 304, 3rd floor of Izumi Ward Office | 045-800-2351 | iz-zeimu@city.yokohama.lg.jp |

| Isogo Ward | 34th floor, Isogo Ward Office, 3rd floor | 045-750-2352 | is-zeimu@city.yokohama.lg.jp |

| Kanagawa Ward | 325 on the 3rd floor of Kanagawa Ward Hall Main Building | 045-411-7041 | kg-zeimu@city.yokohama.lg.jp |

| Kanazawa Ward | 304, 3rd floor of Kanazawa Ward Office | 045-788-7744 | kz-zeimu@city.yokohama.lg.jp |

| Konan Ward | 31st floor, Konan Ward Office, 3rd floor | 045-847-8351 | kn-shiminzei@city.yokohama.lg.jp |

| Kohoku Ward | 31st floor, Kohoku Ward Office, 3rd floor | 045-540-2264 | ko-zeimu@city.yokohama.lg.jp |

| Sakae Ward | 30th floor, 3rd floor of Sakae Ward Hall Main Building | 045-894-8350 | sa-zeimu@city.yokohama.lg.jp |

| Seya Ward | 33rd floor, Seya Ward Office, 3rd floor | 045-367-5651 | se-zeimu@city.yokohama.lg.jp |

| Tsuzuki Ward | 34th floor, Tsuzuki Ward Office, 3rd floor | 045-948-2261 | tz-zeimu@city.yokohama.lg.jp |

| Tsurumi Ward | No. 2 on the 4th floor of Tsurumi Ward Office | 045-510-1711 | tr-zeimu@city.yokohama.lg.jp |

| Totsuka Ward | 72th floor, Totsuka Ward Office, 7th floor | 045-866-8351 | to-zeimu@city.yokohama.lg.jp |

| Naka Ward | 43rd floor on the 4th floor of Naka Ward Office Main Building | 045-224-8191 | na-zeimu@city.yokohama.lg.jp |

| Nishi Ward | 44th floor, Nishi Ward Office, 4th floor | 045-320-8341 | ni-zeimu@city.yokohama.lg.jp |

| Hodogaya Ward | 26th floor, 2nd floor of Hodogaya Ward Hall Main Building | 045-334-6241 | ho-zeimu@city.yokohama.lg.jp |

| Midori Ward | 35th floor, Midori Ward Office, 3rd floor | 045-930-2261 | md-zeimu@city.yokohama.lg.jp |

| Minami Ward | 33rd floor, Minami Ward Office, 3rd floor | 045-341-1157 | mn-zeimu@city.yokohama.lg.jp |

Inquiries to this page

Tax Division, Chief Tax Department, Finance Bureau (I cannot answer consultations on individual taxation details and declarations.) Please contact your ward office Tax Division.)

Telephone: 045-671-2253

Telephone: 045-671-2253

Fax: 045-641-2775

Email address: za-kazei@city.yokohama.lg.jp

Page ID: 890-568-032