Here's the text.

Financial Glossary

Last Updated March 13, 2024

In order to make the financial publicity easier to understand, "That? What does this mean?" I will explain difficult financial terms in an easy-to-understand manner.

A line

- General Account (Ippenkaikei)

- Borrowing balance corresponding to the general account (Ippenkaikeieikaikaikaikaikaikinzaikan)

- General revenues (Ippanzaigen)

General Account (Ippenkaikei)

Accounting that provides basic administrative services such as welfare, medical care, education, and maintenance of roads and parks.

City taxes are mainly used in this general account.

- FY2024 General Account Budget

¥1,915.6 billion (initial budget proposal)

Related Terms

Borrowing balance corresponding to the general account (Ippenkaikeieikaikaikaikaikaikinzaikan)

In addition to the municipal bond balance in the general account, the municipal bond balance in the special account, public enterprise account, and the affiliated group borrowing balance other than the amount to be repaid by the business income of each account (= the amount to be repaid with city taxes, etc.) .

<Included in the balance of borrowings corresponding to the general account>

- General account municipal bond balance

- Of the municipal bond balances in special accounts and public enterprise accounts, those that need to be repaid from the general account as repaid with city taxes due to changes in national standards and social conditions, etc.

- Of the borrowings of affiliated organizations, the city promises to buy later, borrowed to acquire land or create facilities such as roads and buildings.

- Loan balance corresponding to the general account as of the end of FY2022

¥3,114.2 billion

General revenues (Ippanzaigen)

The income that the city can freely decide how to use it.

The main ones are city taxes.

Related Terms

A line

- Fund (Kikin)

- Compulsory expenses (Gimukaihi)

- Cash paid out

- Current account balance ratio

- Prefectural expenditure (Kenshishutsukin)

- Prefectural tax grant (Kenzeikofukin)

- Consolidation Ratio (Kenzenka Solder)

- Public enterprise accounting (Koeikyokaikei)

- Debt service (Kosaihi)

- National treasury disbursements

Fund (Kikin)

The savings of local governments. For each purpose, reserves and reversals are carried out.

In order to install it, it is necessary to specify in the regulations.

<Main of the Funds>

- Financial Adjustment Fund

Funds set to adjust the imbalance of financial resources during the year.

Use it as a source of financial resources when financial resources are insufficient due to changes in economic circumstances, disasters, expenses for large-scale construction projects, and other expenses caused by unavoidable reasons. - Debt Reduction Fund

Funds established in preparation for future redemption of local bonds (municipal bonds). - Other Funds

It is called a special purpose fund. Each purpose is defined.

Compulsory expenses (Gimukaihi)

Expenses that combine the three of the general account expenditures: "personnel expenses", "assistance expenses", and "public debt expenses".

This refers to fixed expenses that must be spent every year.

Related Terms

Cash paid out

Expenses to be spent on special accounts and public enterprise accounts from general accounts according to certain rules.

One of the categories of "by nature" of expenditure.

Current account balance ratio

Every year, how much general revenues (city taxes, ordinary allocation taxes, local transfer taxes, etc.) are allocated to “recurring expenses” such as personnel expenses, assistance expenses, and public loan expenses. An index that indicates whether it is being done.

The higher the ratio, the "general revenue that is expected to generate income on a recurring basis" is used for "recurring expenses", and can be used for other than recurring expenses (for example, facility maintenance expenses, etc.). It can be said that there is little money (the situation where finances are rigid).

- Fiscal 2022 Results

97.9%

If the current account balance ratio exceeds 100%, "recurring expenses" cannot be covered by "general revenues that are expected to generate ordinary income" (≒ temporary financial resources such as withdrawal of funds) ).

It is on the rise nationwide due to an increase in aid costs.

Prefectural expenditure (Kenshishutsukin)

Money issued by the prefecture specifying how to use it for specific businesses based on the provisions of laws and regulations or the necessity of measures of the prefecture.

There are contributions, commissions, incentives for specific measures, or subsidies for financial assistance.

Prefectural tax grant (Kenzeikofukin)

A part of the tax collected as prefectural tax is issued to municipalities based on the law.

There are "local consumption tax grant", "environmental performance grant", "light oil take-off tax grant", "interest rate grant", "dividend rate grant", etc.

Consolidation Ratio (Kenzenka Solder)

Based on the "Law Concerning the Financial Soundness of Local Governments" enacted in 2007, it is a financial index that requires calculation and publication for each fiscal year's financial results.

There are the following four indicators.

- Real deficit ratio

Percentage of deficit such as general account to total income for one year.

If there are no numbers, it indicates that there is no deficit accounting. - Consolidated real deficit ratio

Percentage of deficit in all accounts to total income for one year.

If there are no numbers, it indicates that there is no deficit accounting. - Real debt service ratio

Percentage of repayment of borrowings paid in one year to total income for one year.

The smaller the number, the less the burden of repayment of loans. - Future burden ratio

Percentage of debt repayments paid by the city in the future to the total income for one year.

The smaller the number, the less burden in the future.

When any index reaches the early consolidation standard, it becomes an "early consolidation organization", and there is an obligation to formulate and publish a fiscal consolidation plan.

When any index reaches the fiscal rehabilitation standard, it becomes a "fiscal rehabilitation organization", which requires the formulation and publication of a fiscal rehabilitation plan, and in principle, local bonds cannot be issued.

- Fiscal 2022 Results

- Real debt service ratio

9.7% - Future burden ratio

129.2% - Real deficit ratio and consolidated real deficit ratio

Not applicable

- Real debt service ratio

Related Terms

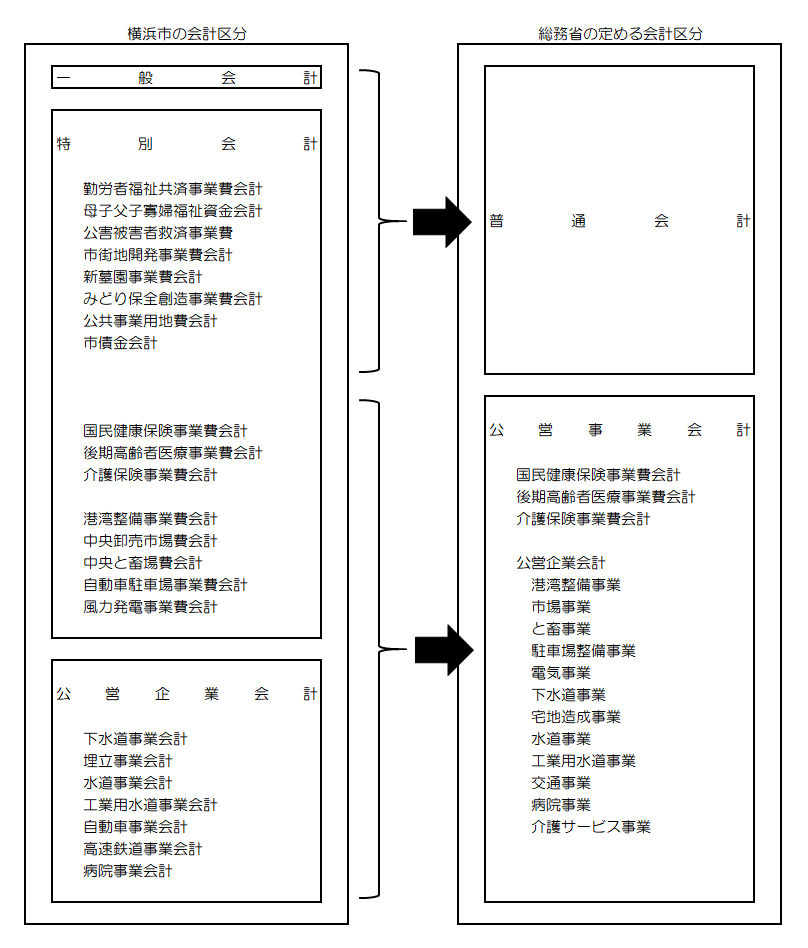

Public enterprise accounting (Koeikyokaikei)

Accounting that manages revenues from business operations as financial resources, just like private companies such as subways, buses, waterworks, and hospitals.

There are seven public enterprise accounts in Yokohama City.

- Sewerage Business Accounting

- Landfill Business Accounting

- Water supply business accounting

- Industrial Water Supply Business Accounting

- Automobile Business Accounting

- High-speed railway business accounting

- Hospital Business Accounting

Debt service (Kosaihi)

Money required for repayment of local bonds (municipal bonds in Yokohama City), which are debts made by local governments.

Includes principal and interest, fees related to issuance and repayment of municipal bonds, etc.

One of the categories of expenditure by nature.

National treasury disbursements

Money issued by the government, specifying the way of use based on the idea of the cost burden of the national and local governments.

There are contributions, commissions, incentives for specific measures, or subsidies for financial assistance.

A line

- Financial Responsibilities Ordinance

- Debt-paying act

- Further deficit local bonds (COVID-19 countermeasures) (further Akaji Hosaisai))

- Fund shortage ratio (Shikin Fusokuhitsu)

- Municipal bonds (shisai)

- Facility maintenance costs (Shisetsu Toseibihi)

- Real debt service ratio (JST)

- Future burden ratio (Shorai Futan Hiritsu)

- Personnel expenses (Jinkenhi)

Financial Responsibilities Ordinance

The official name is "Yokohama City Ordinance on Promotion of Responsible Financial Management for the Future" and was promulgated and enforced in June 2014.

For the purpose of promoting responsible financial management in the future, in addition to the basic principles on the financial management of the city and the responsibilities of the mayor, council, and citizens, the necessary items for financial management are determined. It is intended to balance the promotion of measures and the maintenance of financial soundness.

Related link

Debt-paying act

A budget that goes through a resolution of Congress as a budget to conclude a contract (debt burden) for businesses that need to be spent in the following fiscal year, such as when the construction period spans multiple years.

One of the exceptions to the Principle of Fiscal Year Independence.

Regarding the setting of debt obligations, it is necessary to determine matters, period, and limit as budgets.

Further deficit local bonds (COVID-19 countermeasures) (further Akaji Hosaisai))

Municipal bonds that have been used in addition so that citizens' lives and the city economy will not be hindered due to a significant decrease in tax revenues due to the effects of COVID-19 infection.

| 2020 | 2021 | 2 years | |

|---|---|---|---|

| Decrease in revenue | 69 | - | 69 |

| Special grace bonds | 31 | - | 31 |

| Extraordinary financial measures bonds | 81 | 279 | 360 |

Total | 181 | 279 | 459 |

Note:…It does not match the total because it is rounded to each item.

Related Terms

Fund shortage ratio (Shikin Fusokuhitsu)

Based on the "Law Concerning the Financial Soundness of Local Governments" enacted in 2007, it is a financial index that requires calculation and publication for each fiscal year's financial results.

It calculates the ratio of the shortage of funds to the business scale for each public enterprise for one year.

If the ratio reaches the management soundness standard (20%), there is an obligation to formulate and publish a management soundness plan.

- Fiscal 2022 Results

Yokohama-shi Not applicable

Related Terms

Municipal bonds (shisai)

Loans from Yokohama City. Local government borrowings are referred to as "municipal bonds" and are also referred to as "municipal bonds."

One of the "revenue budget."

Money borrowed for long-term maintenance of public facilities such as roads and parks, and for the conservation renewal project.

- 2024 General Account Municipal Bond Issuance Amount

¥106.6 billion (initial budget proposal)

Related Terms

- Borrowing balance corresponding to the general account (Ippenkaikeieikaikaikaikaikaikinzaikan)

- Further deficit local bonds (COVID-19 countermeasures) (further Akaji Hosaisai))

- Yokohama-style primary balance (Yokohama-hoshiki's Prai Maribaransu)

- Temporary Financial Measures Bonds

Facility maintenance costs (Shisetsu Toseibihi)

Expenses required for maintenance, maintenance, repair, earthquake resistance, etc. of citizen use facilities, roads, parks, etc.

There are many businesses that can utilize municipal bonds.

One of the categories of expenditure by nature.

Real debt service ratio (JST)

Percentage of repayment of borrowings paid in one year to total income for one year.

The smaller the number, the less the burden of repayment of loans.

Related Terms

Related link

Financial commentary (30 seconds commentary on budget and finance) Development

Future burden ratio (Shorai Futan Hiritsu)

Percentage of debt repayments paid by the city in the future to the total income for one year.

The smaller the number, the less burden in the future.

Related Terms

Related link

Financial commentary (30 seconds commentary on budget and finance) Development

Personnel expenses (Jinkenhi)

The sum of employee salaries and retirement allowances.

One of the items of classification by nature of expenditure and one of mandatory expenses.

Related Terms

A line

- Local allocation tax (Chiho Kofuzei)

- Local transfer tax (Chihojo)

- Local special grant (Chiho and Kureikofukin)

- Special Accounts (Special Accounts)

- Specific financial resources

Local allocation tax (Chiho Kofuzei)

In order to adjust the difference in local tax revenue caused by differences in the situation of each region, the government does not have sufficient financial resources for income tax, corporate tax, liquor tax, consumption tax, and tobacco tax among national taxes. What is issued to local governments.

There are "ordinary allocation tax" issued based on a certain calculation, and "special allocation tax" issued according to disasters and other special financial demands.

Related Terms

Local transfer tax (Chihojo)

Tax sources, which should be a local tax, are collected by the government as national taxes, and then issued to local governments.

There are "local volatile oil transfer tax" and "automobile weight transfer tax".

In fiscal 2019, a new “Forest Environment Transfer Tax” was added.

Local special grant (Chiho and Kureikofukin)

Granted by the government to compensate for the decrease in local taxes due to national policies such as tax cuts.

Special Accounts (Special Accounts)

Accounting that performs a specific business with a specific income and makes it independent of the general account to clarify the balance.

There are 16 special accounts in Yokohama City.

- National Health Insurance Operating Expenses

- The Long-term Care Insurance Operating Expenses

- Medical expenses for late-elderly medical care

- Port and Harbor Development Project Cost Accounting

- Central wholesale market expense accounting

- Central and slaughterhouse expense account

- Maternal and child father and son widow welfare fund accounting

- Worker welfare mutual aid operating expenses account

- Pollution victim relief expense account

- Accounting for Urban Development Projects

- Car parking expense account

- New Graveyard Operating Expenses

- Wind power generation expense accounting

- Midori conservation Creation Project Cost Accounting

- Accounting for public works land expenses

- Municipal bond accounts

Specific financial resources

Income that is determined in advance. Major items include national treasury disbursements issued by the government for specific projects, and usage fees for facilities in Municipal Housing and city.

Related Terms

A line

A line

Relief expenses (Fujiyohi)

Expenses required mainly for welfare and medical care, such as the operation of Child Allowance, social security, nursery schools and kindergartens and assistance from medical expenses.

It is increasing nationwide due to the need to promote efforts to support children and child care, and the effects of the progress of a super-aging society.

One of the items of classification by nature of expenditure and one of mandatory expenses.

Related Terms

Ordinary accounts (normal)

One of the accounting categories set by the Ministry of Internal Affairs and Communications.

Since the scope of businesses to be accounted for in each account, such as general accounts and special accounts, differs for each local government, it is a division that is organized based on uniform standards so that comparisons between local governments can be made.

General Accounts

Supplementary budget (Mr. Hoseiyo)

A budget that increases or decreases the initial budget in order to respond to the occurrence of disasters that occurred in the middle of the fiscal year or the revision of laws after the initial budget is established.

If the City Counsil cannot be convened in an emergency, the supplementary budget may be compiled byCity Counsil's decision.

Line

A line

Contingency (Yobihi)

Expenses to cover a budget shortage due to unforeseen circumstances, such as economic fluctuations and sudden disasters.

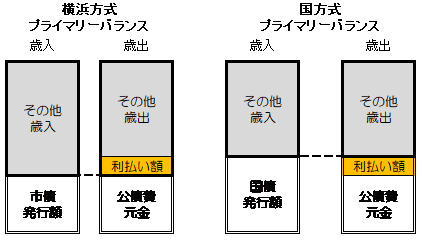

Yokohama-style primary balance (PB) (Yokohama-hoshiki's Prai Maransu)

The idea of keeping the issuance of municipal bonds within the range of the debt service principal (of the debt service, the principal portion) for the year.

It is an idea of utilizing municipal bonds that can prevent the municipal bond balance from increasing by not borrowing new more than the amount to be repaid.

In other words, the idea is that expenditures other than debt service principals are covered by city tax revenues.

Primary balance

Municipal bond issuance amount <The state of debt service principal is “Yokohama method PB surplus”

Municipal bond issuance = The state of debt service principal is “Yokohama method PB equilibrium”

Municipal bond issuance amount>The state of the debt service principal is referred to as the "Yokohama PB deficit."

The government also has a concept of primary balance, but since the private sector type PB is an idea of issuing government bonds within the range of "debt service principal + interest payment amount", the government bond balance will increase by the amount of interest paid.

Since the Yokohama-style PB does not increase the municipal bond balance, it can be said that the standard is stricter than the national PB.

A line

Temporary Financial Measures Bonds

Local bonds borrowed by local governments instead of the money allocated by the government as local allocation tax (from FY2001).

In other words, a portion of the original local allocation tax is covered by the issuance of local bonds.

For this reason, the money for repayment is to be added to the calculation of future local allocation tax.

Related Terms

- Local allocation tax (Chiho Kofuzei)

- Further deficit local bonds (COVID-19 countermeasures) (further Akaji Hosaisai))

Wagon

Reference link

Financial commentary (30 seconds commentary on budget and finance) Basic

Financial commentary (30 seconds commentary on budget and finance) Development

Inquiries to this page

Finance Division, Finance Bureau Finance Department

Telephone: 045-671-2231

Telephone: 045-671-2231

Fax: 045-664-7185

Email address: za-zaisei@city.yokohama.lg.jp

Page ID: 689-305-572